How Edinburgh is maximising revenue per available bed (RevPAB)

By: Kelsey Fenerty, STR

Finding the precarious balance between driving occupancy and driving rate can be a hostelier’s white whale. Not infrequently, markets will drop rate to drive bed sales. Edinburgh has taken a different approach: the market has increased rate despite decreasing occupancy, resulting in higher revenue per available bed (RevPAB).

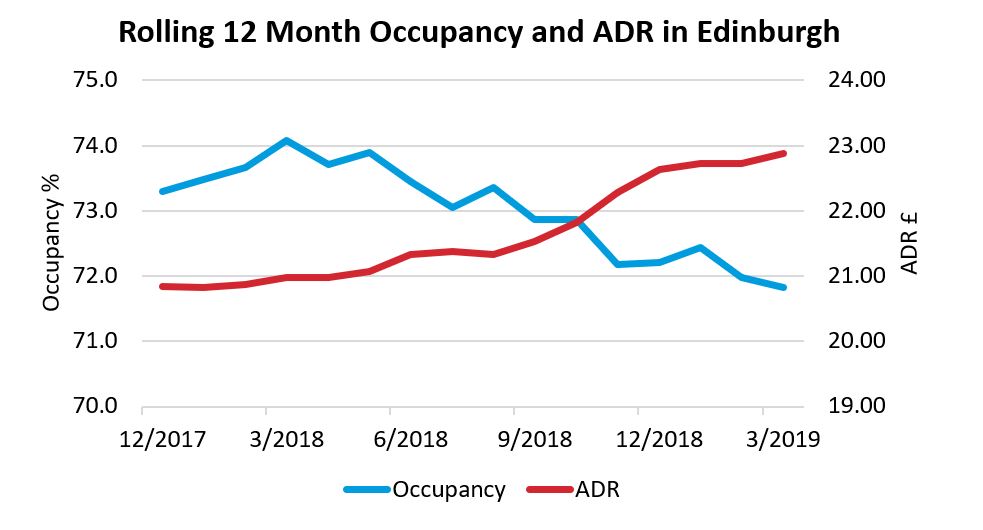

On a rolling 12 month basis, Edinburgh hostels have lost occupancy year-over-year for the past four months, with March 2019 occupancy falling 3.1% to 71.8%. Rate, on the other hand, has skyrocketed, growing 9.1% year-over-year to land at £22.88 in March 2019. RevPAB has increased 5.7% as a result.

ADR has grown in excess of occupancy’s decline for the past four months, suggesting that this phenomenon may be a trend for the market’s hostels.

A look at Edinburgh hotels

Economy and midscale class hotels in Edinburgh have experienced similar declines in occupancy over the past four months, falling 2.4% year-over-year for the 12 months ending March 2019. Unlike hostels, however, hotel rate fell along with occupancy, losing 0.3% compared to March 2018. Hotel revenue per available room has fallen year-over-year for the past four months, as sluggish ADR growth was unable to offset the loss in occupancy.

Part of the hotel slump could be caused by supply growth. As of March 2019, economy and midscale class hotel room supply grew 5.5% year-over-year, which undoubtedly put pressure on occupancy. This would suggest that the market’s hostels are intentionally prioritising ADR growth over occupancy growth.

Capital city comparison

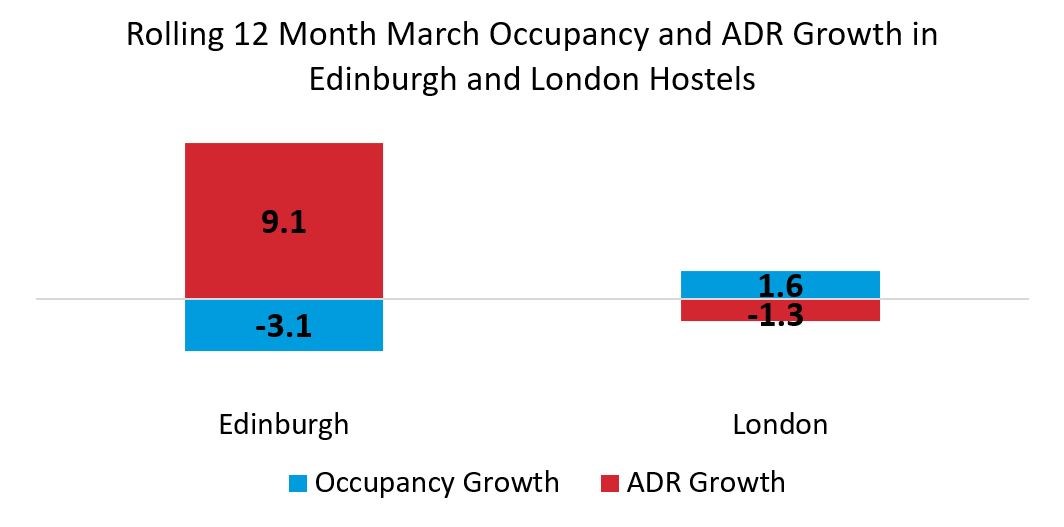

Hostel occupancy in Edinburgh and fellow UK capital London is over ten percentage points apart, with London hostel occupancy reaching 83.4% for the 12 months ending March 2019 compared to Edinburgh hostels’ 71.8% occupancy. Despite the discrepancy, RevPAB between the cities is nearly identical, with London hostel RevPAB coming in at £16.44, just above Edinburgh hostel RevPAB of £16.43.

A closer look at rolling 12 month occupancy and ADR growth patterns sheds light. London hostel ADR has fallen an average of 3.3% as occupancy has risen on average 1.7% year-over-year for the past four months. Meanwhile, Edinburgh hostels added more than 8% year-over-year to ADR for the past four months while losing between 1.4% and 3.1% occupancy over the same time period.

The figure below illustrates the two cities’ strategies, as London hostels prioritise occupancy and Edinburgh hostels prioritise rate.

Prioritising rate may not be the most common hostelier strategy, but it appears to be paying off in Edinburgh.

Interested in more?

STR reports on hostel performance in London and Amsterdam and is actively pursuing other markets. Reports are free to data providers. Interested in more information? Please contact Patrick Mayock at pmayock@str.com.

About STR

STR provides clients from multiple market sectors with premium, global data benchmarking, analytics and marketplace insights. Founded in 1985, STR maintains a presence in 15 countries with a corporate North American headquarters in Hendersonville, Tennessee, USA, and an international headquarters in London, England. For more information, please visit str.com.